|

Work better. Live better. |

|

After making the previous changes to the finances of my business over the past 2 years, I've been able to see a decrease in my expenses of about 30%, and an increase in my profit margin by about 12%. It wasn't nothing and I'm sure glad that I was able to implement those changes when I did.

The next phase of financial reform in my business is something I just implemented...

0 Comments

One the final key pieces that I changed in my business when I attempted to overhaul the way money worked in my painting business was changing to weekly invoicing.

In the past I would take a large deposit - 25 to 50%, a progress payment on large projects, and final draw upon completion. I operated that way for 12 years or so. As mentioned in part one, the large deposit carries risk for both the homeowner and myself as the business owner. The large span between deposit and final payment also caused stress on cash flow because I often have little control on the project. There were times where general contractors would botch the scheduling or change specs and there went my profit. Other times homeowners would take 12 months to complete the other trades prior to me returning for final coat. Even with a 50% deposit, most of that goes to paint and materials, other job costs like fuel, business operating expenses and a little bit of labour. So I quickly found myself upside down on projects and that could last several months sometimes. Not ideal... The decision to stop accepting large deposits had a ripple effect on the finances of my business in many ways.

The most significant adjustment that resulted was that I was no longer comfortable purchasing paint for my client's projects. It was too risky. Customers frequently change their mind, delay their projects, do it themselves, hire someone else, stop returning phone calls, or are indecisive about colours and sheens. So with no or minimal deposits, it freed me from purchasing paint. This is a big change for a painting business. Most painting companies include paint in their quotes. This way they have more control over the materials they use and it can make things more convenient for the client. But does it have to be this way?... In January 2017 I implemented some changes to the way I was operating my business, particularly how money was to be handled.

Partly out of necessity, partly to optimize, and partly as an experiment. I had been doing business the same way for the previous 13 years and I was in a rut. Time for a shake up. After nearly 2 years I can now look back and see if those changes stuck and how they affected my business. The first financial change I implemented was... You know how there are certain author's you look forward to reading all their books...well I think Steven Pressfield's non-fiction books are up there for me. His very popular book The War of Art made a big impact on me and it is essential reading for anyone creating something new that they care about deeply - a business, a book, a work of art, etc.

Since then I've read several other books of his that expand on the concepts in The War of Art. Just finished Turning Pro and I wanted to share one of my big take-aways that relates to running a business... I've been thinking lately that a transaction between a home owner and a painting contractor is a very meaningful exchange, perhaps more than most other transactions.

In a previous post I've discussed that what we, as independent painting contractors, are in the trust business. I still believe that. I still believe that what clients are looking to buy is trust - trust that you know what you are doing, that you can solve their problem effectively, that you can join the family for a couple of weeks. Home owners need to trust you with their money, access to their home, care of their valuables and assets, safety of their family members, their schedule, etc. That is a lot of trust that they are shopping for. And all that trust has a high value to them - they are willing to pay a premium to deal with a company or craftsman they have confidence in. But I no longer believe that what we are selling is trust. We should be marketing trust, our customers should be buying trust, but that is not what we are selling - the thing that we are exchanging for money is not trust, but it is even more valuable... On this rainy West Coast Sunday morning I'm thinking about how many contractors I have personally talked to over the years that have told me that they grew their business to sometimes 2 or 3 dozen people, only to hit a major crisis (health, family, bankruptcy, lawsuit, etc) and decide to scale back, way back, to just themselves and a helper. Like a cool Sunday morning rain, running a small business is just more laid-back. Small is low risk. Small is low stress. Small is manageable. Small is profitable. Small is freedom... Having your own business requires a lot of different insurances. You likely have vehicle insurance for your service truck, WCB, and liability insurance in order to get work. Outside of those basic policies, you may also have tool insurance, home insurance, health insurance, accident insurance, critical illness insurance, or life insurance. But which one is the most important insurance to carry?...

If thinking of buying a home and of starting a business in the near future, it might be prudent to get the mortgage sorted while still steadily employed. Starting a business or financing a vehicle can be done anytime, but it is not always easy to obtain a mortgage. Doing things in the right order can help one reach goals years earlier.

If already self-employed, all hope of owning a home is not lost. Self-employment does make a lot of things in life more challenging, but by now you and I have honed our skills to become tenacious and creative problem-solvers! Here are a few layman tips to increase the chances of approval. Use at your own risk. 1. Maintain a very good credit rating. Fix what you can, pay off outstanding and overdue accounts. If you need to improve your credit score, consider an RRSP loan. Most institutions will automatically approve RRSP loans where the funds are invested in a bank product. Make the loan payments regularly. Use the contribution to reduce your taxable income, this will generate a lower tax bill or a refund come tax time. Take the tax savings and pay down your loan, or keep building up that down payment. Once you are ready to buy, you can borrow your RRSP money to use as a down payment if you are a first time purchaser. In Canada you have 15 years to repay the money to your RRSP account. If you fail to do so you will need to repay the income tax to the government. 2. Save up a down payment. For most people a 5% down payment may be sufficient to qualify, but if you are self-employed and show lower income, or have less than ideal credit, you may need to have 10% or 20% to put down in order to get approved with a competitive interest rate. It is also wise to account for closing costs on your purchase, which can add up to a few thousand dollars. And don't forget moving and improvement expenses, hook-up fees, etc. A sound financial move would be to save 20 - 50% of the cost of your property as a down payment, and choose a shorter term mortgage of 10 to 15 years. Who wants to be in debt for 30 years? That is a huge burden to carry and it can restrict your choices in life. 3. Stay up to date with your financial statements - bookkeeping, income taxes, GST, NOAs, etc. Being able to show the stability of your business over several years and being up to date with your taxes will go a long way. 4. Find the right professionals to help you: So one day about 8 years ago I went to a client's summer home to continue an exterior painting project. It was mid morning and the homeowner meets me at the front door with a serious look on her face and a glass of wine in her hand.

"Simon," she says, as she pulls me inside her house by the arm, "today you won't be doing any painting." Uh, OK...?... Welcome back!

Our service trucks and vans work hard. They could be considered our most important tool. We depend on them as transportation to work, as our sales vehicle, our mobile office, storage unit, lunch room, equipment hauler, and maybe for the odd weekend getaway to the woods. Maintenance is important to keep the wheels turning safely and efficiently. With that in mind, I wanted to pass along a simple but effective tip that I learned last year from an experience shop mechanic... With a new year just around the corner, you as a business owner may be thinking about your sales numbers - what they were like this year compared to last year, what next year should look like, etc.

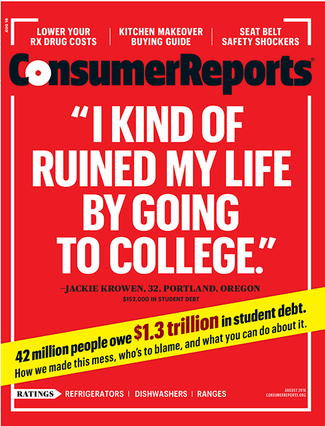

Like the economy, everyone assumes that a healthy business is a growing business. Progress and increase are quick validation that we are working hard and things are going well. If you are not growing you are shrinking, contracting, losing market share, in a recession...all negative sounding things we have been conditioned to have an aversion to. Let's assume for the sake of this blog post that growth is good, necessary even, for your micro-business. We want to measure our efforts and see fine results: higher sales, and more importantly - higher profit...  As a former high school drop out, it is not my place to say that getting a degree is a bad idea. However, it is clear that education is changing fast and that the cost:value ratio of traditional post-secondary institutions is becoming more of a burden than an asset for many students. Technology, industry and economic shifts are developing so fast that a 4-year program is sometimes obsolete by the time you graduate. The skills that seem to be valued in the current job market are adaptability, life-long learning, working with others, project management, entrepreneurial skills, value creation (rather than getting paid to 'show up'), problem solving, social influence and so on. It is a dynamic work-scape out there, with few guarantees or long term commitments on both sides of the employer/employee divide. I'm definitely not an expert on any of these issues. And there is no question that some types of post-secondary training can lead to higher paying work. Having a basic high-school education these days doesn't open a lot of career doors. I just thought it would be practical to think about whether starting a painting business is a viable option for a young person, as opposed to pursuing 'higher education'. The cover story on the August 2016 issue of Consumer Reports stated that 42 million people owe $1,300,000,000,000 in student debt. While many countries around the world offer free education, in North America adult students are drowning in deep pools of debt. Is it a wise investment? Jackie Crowen, aged 32, from Portland Oregon, with $152,000 in student debt is quoted as saying "I kind of ruined my life by going to college." Let's play with some numbers... If she attended school for 10 years, that is an average of $15,000/year in debt. If she had worked instead of attending school during those years, lets assume she could have earned an extra $15,000/year in earnings. That is $300,000 over 10 years that she is behind someone who didn't attend school and started painting full time, earning $30,000/year. How many years will it take her to catch up? If she gets a job paying 50% more because of her education, it would take 20 years! But that is assuming she doesn't end up working at Starbucks, as many highly educated people do. You sometimes end up over-qualified for entry-level professional jobs while lacking experience required for middle-tier professional positions. And that is assuming her skills and education are even still relevant after all that. Now there are other factors to consider... 1. It is unethical. It indicates that you are willing to sell your integrity and honesty for the privelege of working on a project. You don't pay sales tax - it doesn't come out of your pocket, you simply collect it for the governement. So there is little incentive for you to rip off the government. You may feel pressured in order to win the bid, but consider whether you want to work for someone with such ethics. Interestingly, I've had teachers, police officers, Christian clergy and devout Muslims, among others all ask me over the years to 'work for cash', hoping to save 5 - 12% in sales tax. Either you are honest, or your not, simple as that.

2. It is illegal. Do you want audits, fines, assessments, bank accounts frozen, customers contacted by CRA, interest charges, jail time, legal fees, a criminal record? All these are possible consequences of fraud. 3. You never know if it is a test - to see if you are an honest person. Clients are trying to determine if they can trust you with thier most valuable possessions and working around their precious family. Trust is the only thing you are selling. People assume you are a proficient painter...what they want to know is if they can trust you. Trust and honesty go hand in hand. Best to have a solid policy and stick to it firmly and respectfully. You may even be talking to CRA/IRS auditor... Ever wonder if you will be able to retire from painting? By making a few lifestyle changes you can earn your freedom much sooner than most think possible. Pete Adeney is not a painter but his experience of retiring at age 31 may inspire you to adopt some of his strategies...

Little things can make a big difference.

About 4 years ago my brother-in-law gave me a little device called Square that plugs into your smart phone and allows you to accept credit cards. It was a thoughtful little gift. I doubt that I would have tried it out on my own, at least not at that time. Since he bought it for me I felt obligated to set it up. Turns out it was very easy to set up, the device is free to obtain and it is a huge asset to your business if you don't currently accept credit cards. Accepting credit cards helps your business look more professional. Being more profssional leads to closing more deals, at higher margins. Accepting credit cards will help your sales and your cash flow... Just wanted to spread the word on a great banking offer if you live on Vancouver Island...

Island Savings is offering a Simply Free Account that is free to open, has no fees, and they will pay you $50 to open one. If you normally pay an average of $12/month in service charges/fees, this offer equals a savings of $194 in just the first year. We use one. We also use a business account there and save approximately $40/month on that account, compared with what we were paying with a big bank. That is another $480/year in savings! But that is not the main reason we bank there... An observation from the last 12 years of self-employment: The more you charge, the better you are treated. How does that work? I'm not sure, but I would guess a couple things are at play...

A couple of months ago I had a cancellation. As happens from time to time. You just roll with it - because really there is nothing you can do about it, and sometimes it takes the pressure off of an over-booked schedule.

The problem is that it is very easy for a prospect to cancel a job when they haven't made a financial commitment. Unfortunately, as the contractor, you don't have the same flex going the other way. Imagine cancelling at the last minute on a customer - the bad rep you would develop, how you could totally mess up their entire project schedule and that of the other trades, etc... 05/2017 Update: After using Easy Invoice App for over a year and appreciating it's value, I have stopped using it due to a change in their pricing. It may still be a viable option for your business, but for now I have chosen to go back to using a template on my MacBook. A little more work, less utility, but cheaper and not held ransom by a 3rd party app.

The calendar can be an effective agent of change. For the past 11 years I had been generating almost all my sales documents by hand. That means hundreds and hundreds of pages worth of estimates and invoices, all painstakingly hand-written. The thing is, I had experimented with Word and Pages and dabbled with various apps, but nothing seemed to meet my needs. I felt like it was simpler and that it gave my business a craftsman feel. But maybe it was fear of change, laziness to learn a new method, or pure procrastination. Either way, the time had come to try something new. This past January I decided that it was time to commit to switching to digital estimates and invoices. After 2 months of using this particular app to create all my estimates and invoices, I think I found an effective new tool that is an asset to my business. I'd like to share it with you in case you are looking for a simple way to manage this aspect of your business... WHY: TIME IS YOUR REAL CURRENCY

So I've read a couple of brief blog posts lately that have got me thinking... You work hard for your money. I know you do. I paint everyday like you, and I personally know a lot of painters. The cash flow can be pretty good if you are smart and hard working and good with people and a little bit lucky. But the point is you earn your money. What you chose to do with that money is where things get interesting... After over a decade of dealing with a variety of customers and situations, I've learned the hard way to recognize 'red flags' that potentially pose a risk to my business and peace of mind. The best protection I have found is to avoid working for certain prospects and projects. The 3 main red flags that I pick up on are:

1. Unreasonable expectations. A year a half ago I received a phone call that perfectly illustrates this red flag. In the middle of peak season a lady called and asked if we are available to paint the interior of her house in short order. She needed it done in two weeks. But there was a catch - she was on a very tight budget. Normally I like to look at every job, but I didn't think there was any way we could squeeze it in and the low margin was not an incentive to even try. Out of curiously I asked what the size of the house was. She replied 5000 square feet. That was pretty much the end of the conversation. For our small and busy business there was no way we could even think of taking this on. Going any further would have been a complete waste of both of our time. When I started my business I had a very keen desire to help everyone and try to take on every job. This was not modest and it exposed me to quite a bit of stress and risk. As a rule of thumb a job consists of three factors - quality, scheduling and cost. I can usually accommodate 2 out of 3 (as long as one factor is quality). If someone expects all three, or makes other unreasonable demands, it's time to reset expectations or walk away... WHY: FEEL GOOD ABOUT WHAT YOU CHARGE

Earlier this month Seth Godin wrote a brief blog post sharing a simple formula for calculating hourly rates for independent contractors. 'Successful freelancers need to charge at least double the hourly rate that they'd be happy earning doing full time work. (In many fields, it's more like 4 or 5x).' If the average proficient painter can make $20/hour ($40,000/yr) working as an employee, let's see what he should charge for contract work using this principle: $20 x 2.5 = $50/hour That should be your baseline figure. If you or your clients feel that is high - how can you reconcile the cost and feel confident about your ask? One thing you can do is do the math... WHY: DOING IT IS DIFFICULT BUT PROBABLY NECESSARY

Do you frequently find yourself tight on cash-flow? Are you too busy - is your customer service dropping? Are you attracting the wrong customers, ones that are unreasonable? Tired of offering a particular service that you don't enjoy or that offers little profit? Not enough time to pursue the things that are really important to you and your family? The answer to all these problems (and more) might be as simple as raising your prices. It's easy to say, but hard (and scary) to do. On another blog post we will deal with why you should raise your prices. But for now, lets assume you've realized that a price increase is needed. How can you implement your decision? *something to consider before you think about raising prices: Am I as busy as I want to be? If not, raising prices may not be your first priority. Although, low prices may be driving good potential clients away...

|